Revised by

By Robert Hokin, Managing Partner, Fundraising101

I attended the launch of the Scottish Deep Tech Report 2026 this week, produced by Dealroom in partnership with the University of Glasgow. I’ve read it cover to cover and I’ve been thinking about it since. Here’s my honest, detailed take. The link is above, below and here.

First, the headline: this is the most authoritative, data-rich picture of Scottish deep tech we’ve ever had. It deserves serious engagement from everyone operating in this ecosystem: investors, founders, universities, accelerators, government agencies. Read it. Then read the recommendations. Then act on them.

Let’s be clear about what this report actually shows.

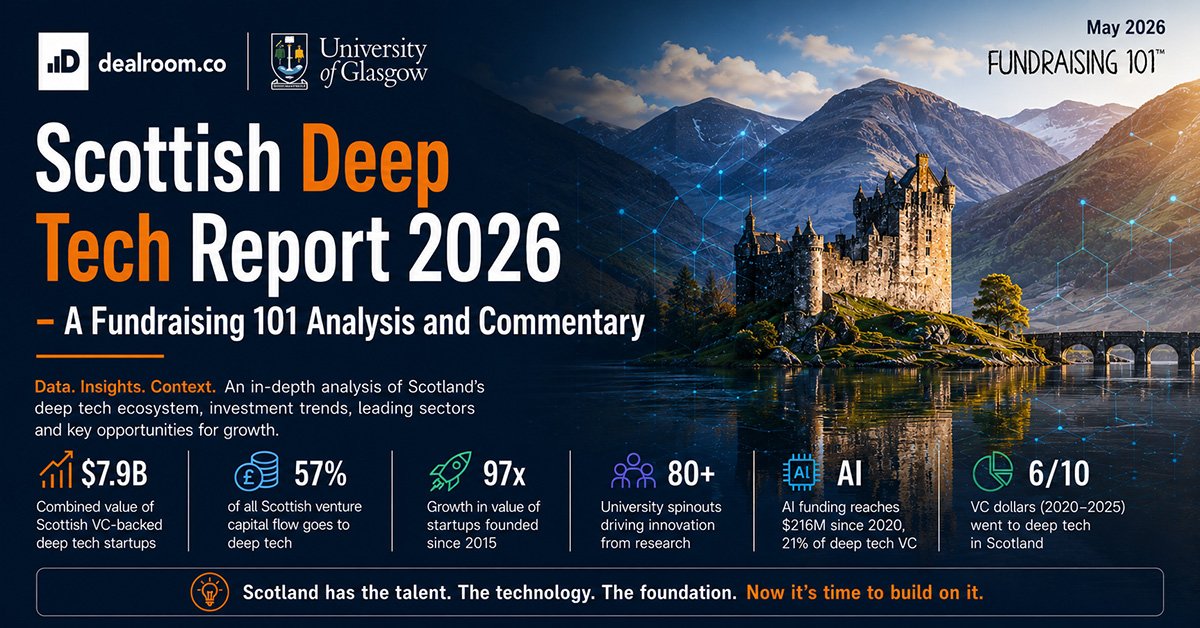

Scotland punches well above its weight in deep tech concentration. Nearly 60% of all Scottish venture capital goes to deep tech; second globally only to Switzerland. Private deep tech startups are now worth a combined $7.9 billion, up 10.7x in a decade. The sector generated $323 million in VC funding in 2025 alone. University spinouts, over 80 of them, account for 43% of all Scottish VC-backed deep tech companies and 56% of total ecosystem value. Four Scottish universities rank in the UK’s top 20 for deep tech spinout activity: Dundee at 6th, Edinburgh at 10th, Glasgow at 13th, Strathclyde at 14th. Against Oxford, Cambridge, UCL and Imperial, that is not modest. That is extraordinary.

The investor base has tripled over the past decade. The sector has produced a unicorn in Exscientia and four revenue-generating colts. Climate tech alone has grown from $278 million to $3.1 billion in enterprise value. Biotech and pharma represent 73 VC-backed companies with $3.7 billion in combined value. The space sector, where Glasgow is the largest small satellite manufacturing hub outside California, has scaled from $4 million to $600 million in enterprise value in under a decade.

All of that is real, and it is worth celebrating.

Now for the harder conversation.

Scotland is not great at startups in the way the ecosystem sometimes congratulates itself. Scotland IS great at early-stage deep tech formation and great at scientific output. It is not yet great at converting that pipeline into scaled, Scottish-owned enterprises. From a base of 260+ active VC-backed companies, only five have reached scaleup status. Companies plateau at 20–30 employees and get acquired, typically by foreign buyers, or stall entirely. Alastair McInroy, CEO of Technology Scotland, captures it precisely in the report: “lots of micro or small SME enterprises at one end, then a small number of large multinational, anchor companies at the other, all foreign owned. There’s really nothing in the middle.”

That pattern has been present for as long as I’ve worked in UK venture and technology investment, more than 30 years. What this report does, for the first time, is document it with precision. That precision is what creates the obligation to act differently.

The five report recommendations deserve serious advocacy. Here they are, and here’s why each matters.

Recommendation 1: Develop deep tech leaders specifically built for scale.

This is the most operationally urgent recommendation in the report. Scotland produces world-class scientists and engineers. It does not reliably produce the commercial leadership needed to take those companies through the difficult transition from 20 employees to 200. Professor Mark Symes of the University of Glasgow identifies the root cause: “In science and engineering, we have individuals with an entrepreneurial mindset, but generally they’re not the best people to be the CEO. My students say ‘I do not want to spin out because I don’t know anything about business.'” The report calls for structured team formation programmes, matching technically brilliant people with commercially fluent operators at the pre-formation stage, rather than trying to retrofit business skills onto scientists who neither want nor need to become CEOs. This is exactly right.

It is also exactly where Fundraising 101 operates: not as a training provider, but as the investment readiness infrastructure that prepares technical founders to communicate with investors on the investor’s terms. We work with the founder who is present, not the founder we wish they were.

Recommendation 2: Build commercial and technical literacy across the full value chain.

The dominant model in Scotland’s deep tech ecosystem trains the founder. The report argues, correctly, that this is necessary but insufficient. Investors need sub-sector depth to make confident Series A decisions. Procurement officers need frameworks to evaluate early-stage deep tech. Supply chain partners need technical literacy to engage with what these ventures actually need from them. Mark Western, Technology Sector Team Leader at Scottish Enterprise, notes in the report that Scotland’s investment community is “quite generalist — willing to have a punt on seed funding, but without the depth of sub-sector knowledge required for Series A type investment.”

This is where Fundraising 101 also has the most direct contribution to make. Our expertise is precisely this: venture financing literacy for both sides of the table. We help technical founders understand how investors think, how deals are structured, and what a credible investment narrative looks like for a capital-intensive, IP-rich, long-development-cycle business. We help founders build the commercial vocabulary that closes the communication gap that kills more funding rounds than bad technology ever does. Covering venture financing, IP strategy, raise structure, investor targeting, and objection framing: this is our daily work. The report calls for it at ecosystem scale. We deliver it at company level.

Recommendation 3: Fix the infrastructure access problem.

The report makes a sharp and underappreciated argument here: Scotland’s infrastructure problem is not one of asset availability. It is one of operating model. World-class fabrication facilities exist. Shared cleanrooms exist. What doesn’t exist in sufficient quantity is infrastructure designed for the 10–50 person company stage: mixed office, lab, and light manufacturing space on flexible terms, with genuine IP protection, priced for pre-revenue companies. The report points to the Science Creates model in Bristol as the reference point: independently operated, financially self-sustaining, built around the needs of a growing company rather than an academic institution. This recommendation requires capital and governance change at institutional level. It will take time. But it is the right call.

Recommendation 4: Make Scotland a first customer for its own innovations.

This is the most systemic recommendation in the report and, if acted upon, potentially the most impactful. Scotland consistently generates deep tech innovation and consistently fails to retain it. Emma Loedel, Senior Enterprise Manager at the Royal Academy of Engineering, puts it plainly: “We are not quick enough to be early adopters of our own innovations. We too often encourage people to go and try things outside of Scotland and then bring it back, but by that point it’s too late, they’ve gone.” The first anchor customer is frequently the decision point between a company staying in Scotland and following the money elsewhere. Scotland’s public sector has significant procurement power across health, energy transition, food and agriculture, and public infrastructure, precisely where its deep tech strengths are concentrated. Using that power as demand-pull innovation infrastructure is not protectionism. It is recognising that anchor customers are infrastructure, and that Scotland is currently exporting that infrastructure by default.

Recommendation 5: Develop a distinctively Scottish understanding of deep tech innovation futures.

Much of Scotland’s deep tech policy conversation is conducted in borrowed language: Silicon Valley benchmarks, unicorn counts, Golden Triangle comparisons. The report argues for something more ambitious: a distinctively Scottish approach to deep tech, built from Scotland’s actual conditions, strengths, and values rather than imported from contexts that don’t apply. Scotland has compact geography, a strong university base, a distinctive policy environment, and existing commitments to a just economy. These are assets, not constraints. The call is for sustained social science research into how deep tech actually functions here, not another report on what Scotland lacks, but rigorous, patient intellectual work on what it actually is.

I agree with this entirely, with one addition. Scotland also needs international credibility at the early stage. Not because San Francisco is the benchmark, but because the investors who fund Scottish deep tech at Series A and beyond are making comparisons to global standards. The report shows this clearly: US capital represents 35% of all $15M+ rounds. Meeting global standards while building a distinctively Scottish model is not a contradiction. It is, in fact, the brief.

How and Where Fundraising 101 supports this report.

We are a pre-seed investment readiness practice. Our work is in the gap between world-class scientific output and investable narrative, the gap the report implies but doesn’t name. We support technical founders on venture financing strategy, raise structure, investor targeting, deck communication, and IP commercial framing. We work across the sectors this report covers: biotech, climate tech, quantum and semiconductors, space, and deep tech AI. We already work in partnership with Scottish Enterprise, Sustainable Ventures & The National Climate Tech Accelerator, Scottish EDGE, IBioIC, and Converge.

The report’s first two recommendations are the ones we are best positioned to support immediately. If you are a founder, accelerator, university commercialisation team, or investor who wants to talk about what investment readiness looks like for a technically complex early-stage venture, that conversation starts at fundraising101.academy.

The Scottish Deep Tech Report 2026 is the evidence base this ecosystem needed. Now the work begins. Let’s get on with it.

Robert Hokin is Managing Partner at Fundraising 101 Academy, a pre-seed investment readiness practice based in Glasgow. He hosts the First Money In podcast and publishes the Dry Powder newsletter.

Get Raise-Ready. Pre-seed tech founder in Scotland? There’s a difference between deck-ready and Raise-Ready. We can help you get there. Fast. With no nonsense. Visit fundraising101.academy.