Written by

Robert Hokin

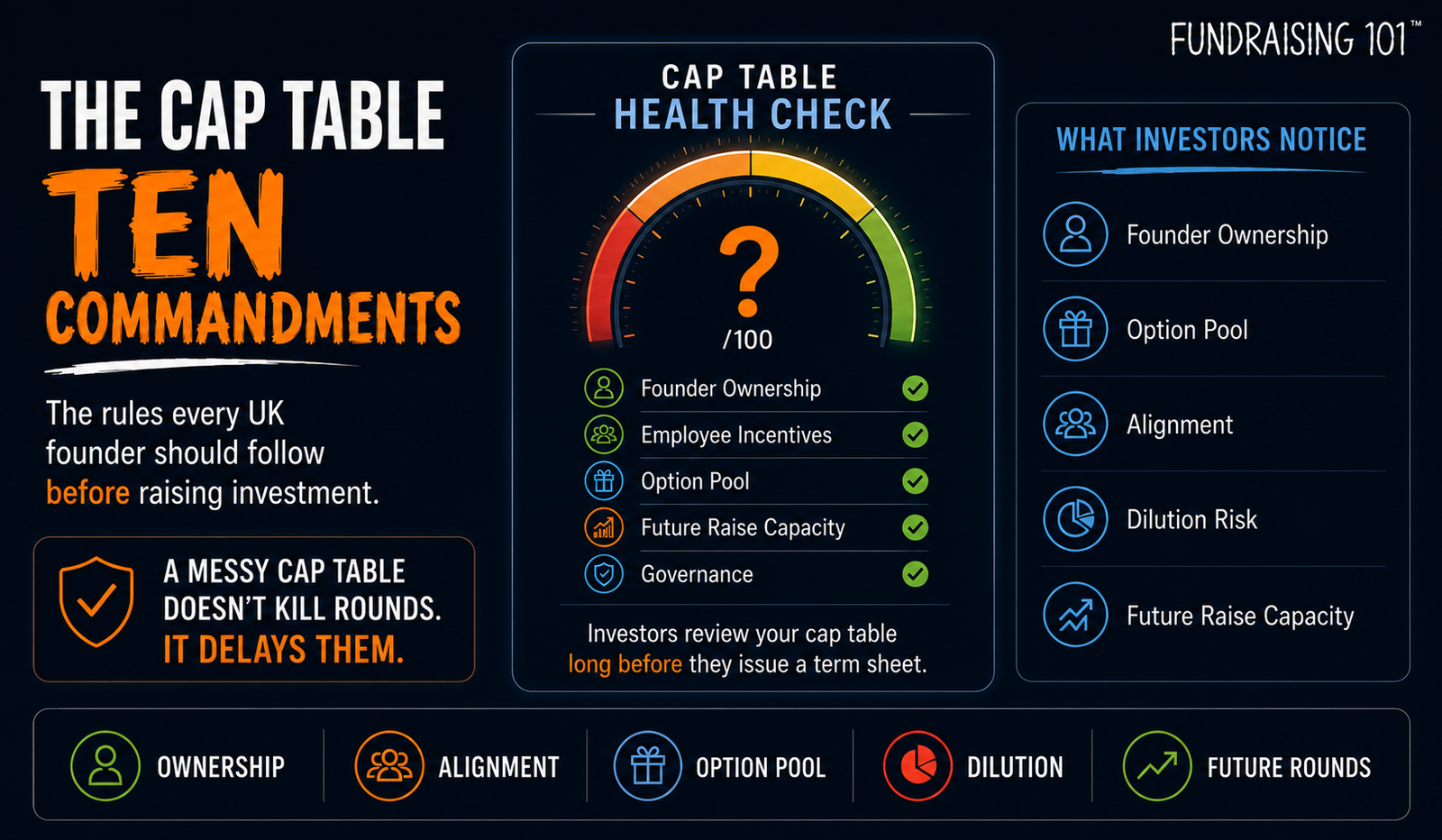

The Cap Table Ten Commandments! Don’t wait to think about your cap table until an investor asks to see it. By then, the mistakes are already baked in.

Your cap table isn’t just a spreadsheet. It defines ownership, incentives, dilution, and how future fundraising plays out. Get it wrong early, and those decisions compound until they become deal-breakers.

Even if it’s your first funding round, I’ve watched strong companies struggle to close Series A—not because of weak products, but because early equity decisions and over-dilution created problems no one modelled. Your cap table defines ownership, incentives, and how future rounds play out. Get it wrong early, and those decisions compound into deal-breakers.

By then, the mistakes are already baked in—and they’re expensive to fix.

These problems are totally avoidable. Here’s how to sort them early on.

The Cap Table TEN Commandments

1. Build it the day you incorporate. From day one, know exactly who owns what—and what that looks like after future rounds. Early clarity prevents late surprises.

2. Put all founders on vesting from day one. Four-year vesting with one-year cliff. Non-negotiable for serious investors. Handle it at incorporation when it’s clean, not later when it’s messy and creates tax issues.

3. Never EVER give more than 0.25-0.5% to advisors, and always include vesting with clear deliverables. Standard is 0.1-0.5% over 2-3 years with quarterly or annual vesting. Anything more than that will trigger serious scrutiny.

4. Always think fully diluted, not issued shares. Fully diluted = issued + options + SAFEs/ASAs + everything promised. When you say you own 60%, investors assume fully diluted. If you mean issued, prepare for awkward conversations.

5. Treat SAFEs/ASAs as real dilution before they convert. They’re not shares yet, but economically they exist. Model all outstanding convertibles and assume worst-case conversion. That false sense of ownership evaporates when you price your next round.

6. Assume the option pool will be topped up—because it always is. It expands at nearly every major round. Plan for it now or face painful renegotiations later with less leverage.

7. Model liquidation preferences across scenarios. 1x non-participating is very different from 1x participating. Model exits at £10M, £30M, £50M to understand when you actually make money. Ownership percentage alone doesn’t tell the story.

8. Clean up BEFORE you raise, not during diligence. Unsigned option grants, verbal agreements, unclear SAFE terms—fix them well before investors look. Nothing kills momentum faster than “we need to sort out cap table issues first.”

9. Plan backward from Series A expectations. UK Series A investors expect founders at 50-70% post-money, 10-15% option pool available, clean structure without messy convertible stacks. Work backward from these expectations when planning pre-seed and seed.

10. Never grant equity without modelling the long-term outcome. Model every grant through Series A and B. If you can’t explain what it looks like after two more rounds, you’re deciding blind. Equity is permanent.

The bottom line: Your first cap table is just that-your first. You don’t know what you don’t know.

Commandment 11! Have an experienced lawyer, CFO, or operator review it before you make irreversible decisions. The £2-3K you spend will save you £50K+ later. Get in touch if you want references to some excellent ones.

Robert Hokin is the Founder in Chief of Fundraising101™ Academy, where he teaches pre-seed Scottish tech startups the DIY fundamentals of effective investment-raising. With 25+ years of UK technology investment experience and 500+ ventures guided through fundraising, he’s seen what works – and what doesn’t.